All the FloBot students get it and can then use it as is or adapt it to their needs. All it does is identify the trend and trades the pullbacks.

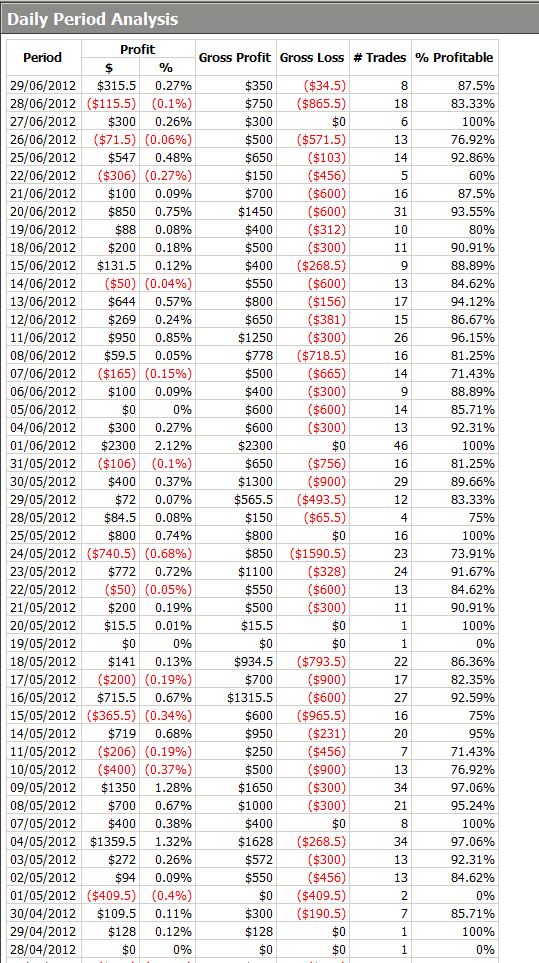

These results are for the period from the end of February until Friday this year. The algo covers 7am until 9pm London time = 2am until 4pm New York time. It is set on a profit of 1 ES point or $50. All entries are LIMIT entries and the backtesting requires that price pass through the limit by at least one tick. Slippage is not a real factor due to the fact it is the ES and the majority of stops would be elected without that problem.

This algo is good to go as it is for me.

$15,000 profit for 1 contract after commissions

Drawdown of less than $2,000

88.87% Win Rate

Over 1,000 trades sample size

But OK, you want to make more money than these stats or to increase the average trade amount or other stat.

What can you do?

Firstly, look at the times of day that there are losing trades. Is there a pattern?

Next, look at the losing trades. Is there a filter that is DYNAMIC (adjusts itself with market changes) that filters out losers?

Then, look how you can increase the 1 ES point $50 target using DYNAMIC exits.

The requirement, after you've done all the work and due diligence, is to leave the algo alone and let it do it's thing.

The results look awesome! Are these figures adjusted for spread/commission? That's a good amount of trades and I've learned that results could easily be affected by such when the profit targets could be equal to or more than cost to play.

ReplyDeleteKemo, they include $6 round trip commission per contract but not slippage as entries are limit orders and exits are stops that should not usually have slippage due to ES size on bid and ask. The walk forward analysis looks great too.

DeleteGreat post EL. what periodicity do you use to get these results? I'm assuming range bars.

ReplyDeleteAnon 20:28 adjusted Renko. MultiCharts has a new way of drawing renko bars with wicks and correct open.

DeleteHi EL,

ReplyDeleteif a profit is set to 1 ES point or $50, how can be the daily profit in onetrade days greater than $50 (04/03/2012, 18/03/2012...)?

DH

DH, Gap between the Close and Open.

ReplyDeleteDo you have it set so that price must also pass through your exits by 1 tick to guarantee closing the position?

ReplyDeleteAnon 12:43. Yes, I want to make the backtesting as disadvantageous to me as possible because the real world will be not nearly as good. catching 50% of the profits of a backtested model is pretty good. I'm usually happy with less.

ReplyDeleteHey there Digger,

ReplyDeleteESs algos very impressive. Can you confirm that I have got it right ,or at least close enough, that there were 9 consecutive winning trades today , 6th July? If not ,can you please confirm the number.

Thanks, David

BTW are you young enough to remember Tasminex, LOL

David, I had 4 winners, then a loser and then a winner. Sure I remember Tasminex. What about VAM.

ReplyDeleteEL - does the algo depend on renko bars or would you get the same or similar results using range bars?

ReplyDeleteThanks,

TB

Hi TB. Good to hear from you again. No, the algo works well with range bars, it's just a bit more profitable on some markets with the renkos with wicks.

ReplyDelete