The guy had a simple philosophy; he made 8 ticks in the T-Bond every day and then hopped into his Porsche and drove down to the beach. That was it. He increased size as he wanted to make more money.

I always thought there was something clever about this but my own work ethic always got in the way and I think/thought that you should keep on working while the market pays you to do it.

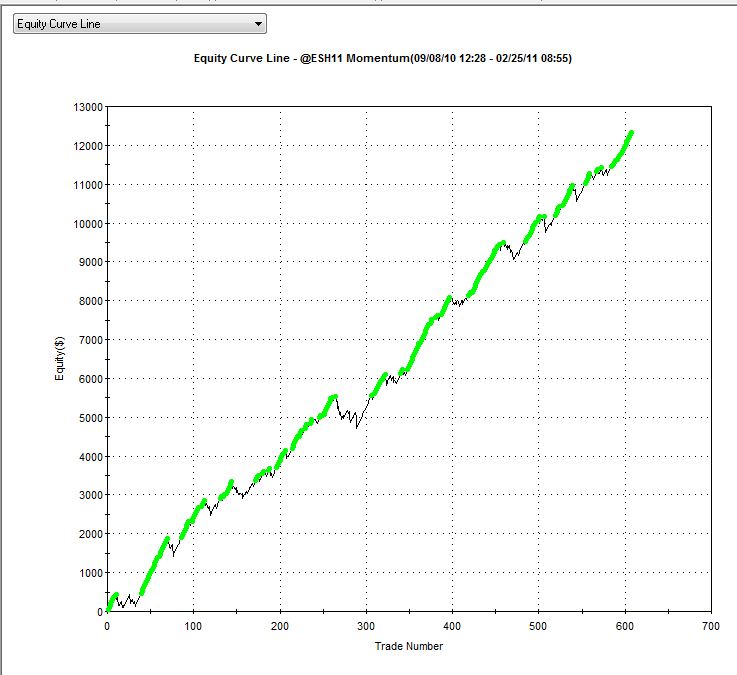

But maybe not. The stats below are taken from a TradeStation optimisation that we ran testing what daily profit and daily loss limit is the best. So many of my students have TradeStation, I opened a TS account again so I can duplicate their trading with the same data. BTW, I'm using what TradeStation calls "Momentum Bars" using the range I want constructed out of 1 tick data. These are most like the Range Bars I am used to in MarketDelta and other charting software.

The stats are quite interesting. The algo, periodicity (3 tick momentum (range) bars) and date range (6 months) and time traded, gave a daily profit limit ($750/contract) more than twice the daily loss limit ($350/contract), a very logical result.

What is even more interesting, I can use this to decide which are the best times of the day to trade in order to get the best stats. In this case, Flo trades from 9.30am NY time (the beginning of RTH) until 12.10pm NY time (2 hours and 49 minutes later). She trades limit orders so if she gets filled and she mostly has, then there is no slippage.

The more I use my FloBot to trade and test, the more I like it as it provides so much information and in fact makes me more money. Using a 'bot can not only bring CP to more people but it can do it much, much more quickly. I can override the exits and make even more by scaling out and using trailing stops. I've programmed that into Flo too and I'll share some ideas about that in later posts.

Summary

Monthly Profitability

Equity Curve

I was trading the ES today. It was an obvious gap day and I was short into the number and picked up a couple of points. I looked to re-short but Flo would have none of it. She just wanted the long side going into RTH. She enforced my discipline. Go Flo!

jenrique42

ReplyDeletees gracioso pero una filisofia muy similar es la que quiero aplicar yo con el dax, sacar unos 200 euros, netos al dia, unos 8 puntos, que vendrian a ser despues de impuestos y de comisiones, como hacer un trade de unos 10 puntos brutos, y con esto me conformaria y podria vivir bastante bien

lo que haga despues el mercado pues no me importaria en demasia

jenrique42

funny, but very similar filisofia is what I want to apply the dax, get about 200 euros net per day, about 8 points, which would come to be after taxes and commissions, such as making a trade of 10 points gross, and by that I could settle and live quite well

what to do after the market because I would not mind in extremis

Interesting... You use momentum bars rather than the range bars they have?

ReplyDeleteCurious - does that report include commish in the figures?

Donald, The TS Momentum Bars are range bars. Their Range Bars are just range bars constructed differently. And yes, I always deduct comish. No slippage as there is none because I enter and exit profitable trades on limit orders and the losers exit at the spread anyway without slippage.

ReplyDeleteHi EL,

ReplyDeleteThanks for posting these results. Very helpful to show what's possible and to set reasonable goals.

Hi Tom, regarding the "porsche guy", let's say that he began his trading day by 2 or 3 losers in a row (stuff happens ;-)

ReplyDeleteWhat was his plan then ? continue trading until he "made" his 8 ticks or quitting for the day ?

Thanks for your time.

Gwen

How did you manage the two long trades around 20:55? Were you stopped out of both or did you exit early with a small loss?

ReplyDeleteEL - You mentioned above that you ENTER using a Limit order which is a departure from your Dicretionary practice of stopping your self into the entry at the End of Bar. Does Flo use the End of Bar price or 1 tick higher (for longs)?

ReplyDeleteWhat is your first Take Profit Price for Flo' Inside-Out trades?

Thanks

R

Gwen, I only saw him make 1 losing trade in a row so don't know the answer. He just made up the loss plus a bit with the trade and called it a day.

ReplyDeletebakrob99, it enters with a limit of the close of the bar that the signal was generated on. It can miss a trade with this but it doesn't happen often and its MUCH cheaper than paying slippage.

Anon 23:43, I wasn't trading as it was past my bed time but had I been, I would have stopped myself out just under the lows of the bar after the second arrow as I would have expected the market to move in my direction immediately in that context.

ReplyDelete